QUEZON CITY -- Given the misconception that the use of the phrase “highest COA audit rating” may cause and its potential impact to decision makers and the public, the Commission on Audit (COA) would like to clarify again that an audit opinion should not be viewed as a rating, score or grade, with ranking of lowest to highest.

An audit opinion pertains only to the financial audit conducted regularly by COA auditors on the agencies within its jurisdiction. It may be unmodified or modified, depending on whether an agency’s financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework.

An unmodified opinion (also referred to as unqualified opinion) is issued when the auditor concludes that the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. Meanwhile, a modified opinion – includes qualified, adverse and disclaimer of opinion - is issued when the auditor concludes that, based on the audit evidence obtained, the financial statements as a whole are not free from material misstatement; or is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement.

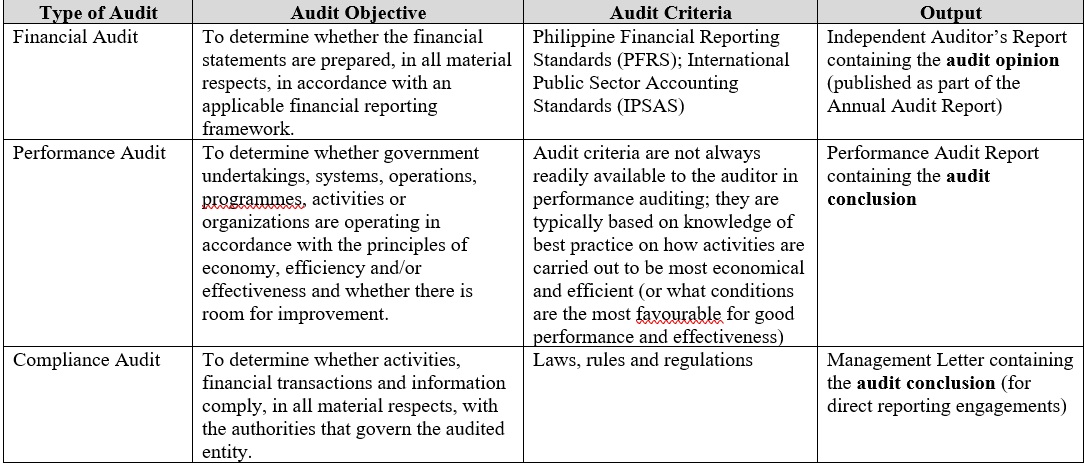

It is important to note that the financial statements represent only a facet of an agency and that an audit opinion does not provide any conclusions on the agency’s level of compliance with laws, rules and regulations, nor the application of the principles of economy, efficiency, and effectiveness in the agency’s operations. Such matters are covered by the compliance and performance audits, respectively, which are conducted by the COA in addition to financial audit.

Results of these audits are found in the Annual Audit Reports and are uploaded in the COA website.

Understanding the Audit Opinion

Based on the powers vested by the 1987 Philippine Constitution, the COA conducts financial, compliance and performance audits. In the conduct of such audits, the COA uses the International Standards of Supreme Audit Institutions (ISSAIs), which are the standards being used by almost all the supreme audit institutions worldwide. The table below summarizes the key differences of these audits:

As the basis for the auditor’s opinion in the financial audit, ISSAIs/ISAs require the auditor to obtain reasonable assurance whether the financial statements as a whole are free from material misstatement, whether due to fraud or error. Reasonable assurance is a high level of assurance. It is obtained when the auditor has acquired sufficient appropriate audit evidence to reduce audit risk (that is, the risk that the auditor expresses an inappropriate opinion when the financial statements are materially misstated) to an acceptably low level.

However, reasonable assurance is not an absolute level of assurance, because there are inherent limitations of an audit which result in most of the audit evidence on which the auditor draws conclusions and bases the auditor’s opinion being persuasive rather than conclusive.

As such an audit opinion only covers the financial audit and thus, does not reflect the agency’s level of compliance with laws, rules and regulations reported under a compliance audit (unless these have financial impact), nor the application of the principles of economy, efficiency, and effectiveness in the agency’s operations reported under a performance audit.

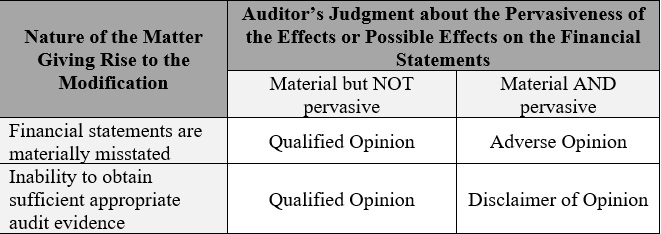

To provide additional information, the following are the different types of opinion issued in connection with financial audit based on ISSAI 2700 and ISSAI 2705 which were crafted from International Standards on Auditing (ISA) 700 and ISA 705:

A. Unmodified opinion (also referred to as unqualified opinion) – this opinion is issued when the auditor concludes that the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework (i.e., PFRS, IPSAS). For this purpose, the auditor’s evaluation includes due consideration on quantitative and qualitative materiality established based on the prescribed COA’s audit guidelines. As such, an unmodified/unqualified opinion does not necessarily mean that there were no misstatements found during the audit nor there were no uncorrected misstatements as at year-end. It is possible that the misstatements found during the audit were already corrected by the audited agency or that the uncorrected misstatements are not material, quantitatively and qualitatively. This does not also entail that the audited agency fully complies with all the laws, rules and regulations, or that the uses of funds on the agency’s programs, projects and activities are economical, effective or efficient.

B. Modified opinion – includes qualified, adverse and disclaimer of opinion. This opinion is issued when the auditor (a) concludes that, based on the audit evidence obtained, the financial statements as a whole are not free from material misstatement; or (b) is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement:

Considering the foregoing definition, purpose and context, an audit opinion should not be viewed as a rating, score or grade, with ranking of lowest to highest. Time and again, an audit opinion is a statement that expresses whether the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework (i.e., PFRS, IPSAS). (COA PIO)